Why Overlooking Europe is a Mistake

Fundraisings from Oaktree, Morgan Stanley, Goldman Sachs, Bain Capital and Invesco

👋 Hey, Nick here. Week one of ‘dad life’ has been successfully navigated. Whilst there have been moments of distress, rapid intervention and effective management have led to swift recoveries. Sentiment remains constructive for the week ahead, although I acknowledge ongoing execution risk.

A big thank you to my top three referers Jade Friedensohn, Arnau Roigé Borda, and Kara Conway. I’ll be sending your Credit Crunch Cereal imminently. If you want to join them, use the link below:

As a reminder, this is the 101st edition of The Credit Crunch. Each week, I write about private credit insights and fundraising announcements. You can read my previous articles here and subscribe here.

🆇 Post of the Week

Nothing says “healthy credit markets” quite like the largest distressed fundraise in history.

📕 Reads of the Week

US banks ❤️ Private capital: US bank loans to private capital firms have risen 30x, from $10bn in 2013 to $300bn in 2023. Link

Brookfield expects to double its credit assets within five years. Link

Bain Capital invested $6 billion across 97 investments in 2024. Its portfolio of 200 middle market companies had a weighted average EBITDA of $46 million. Link

Pimco hits back at private credit critics. “You’re not being paid enough for the liquidity risk you’re taking”. Link

Blackstone is also talking about Multi-Asset Credit. Link

Source: Blackstone See last week if you missed what KKR and Apollo think about Multi-Asset Credit.

The hunt for wealthy Europeans continues and StepStone is launching an ELTIF. Link

Brookfield: Europe’s Enduring Investment Themes. Link

Bloomberg interviewed leading credit managers. My top quote is below: Link

In private equity, you only have to be right about 70% of the time. If you make three times your money on 70% of your investments and lose all your capital on the other 30%, it’s probably a top-quartile fund. In public equities, you’ve got to be right a little over 50% of the time. In venture capital, you’ve got to be right about 20% of the time. Your winners pay for your losers. But in credit, you’ve got to be right about 99% of the time. That takes a different mentality. And so that’s what keeps me up at night. I’m afraid that the asset class has grown to where there is capital flowing to the lowest common denominator, where the culture and the talent are not prepared to deliver on the asset class returns. Link

Joshua Easterly

Co-president, co-chief investing officer and co-founding partner at Sixth Street

📆 Event of the week - Configure Partners Quarterly Update

I’ve covered The Configure Partners’ Quarterly several times (Most recently here).

The team provides in-depth private credit surveys as well as market insights from debt advisory engagements.

Register for the February 19 Webinar here

🇪🇺 Why Overlooking Europe is a Mistake

Given all the recent focus on European fundraising, Pictet has produced two reports on why overlooking Europe is a mistake. Below are my highlights - read the full reports here and here

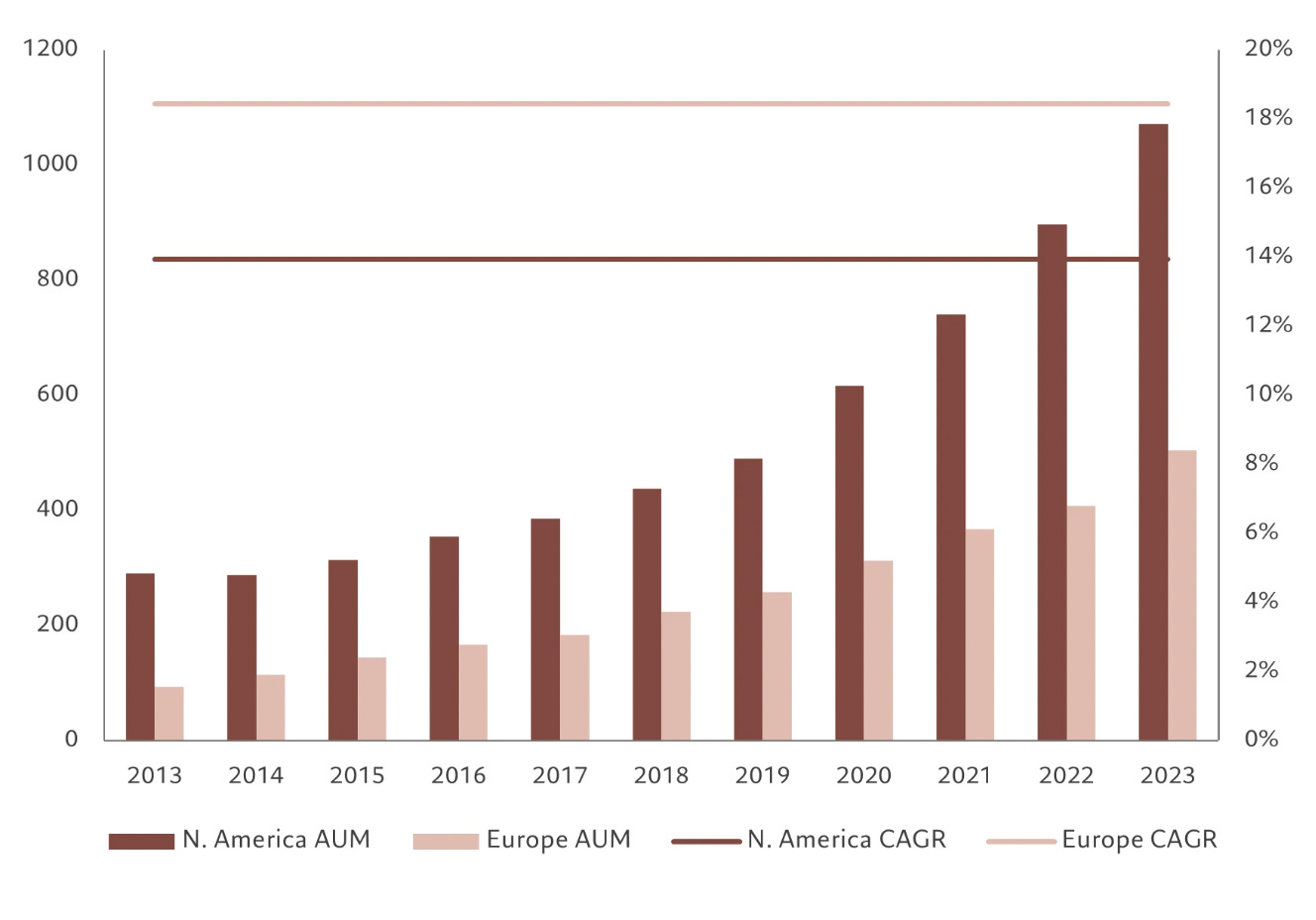

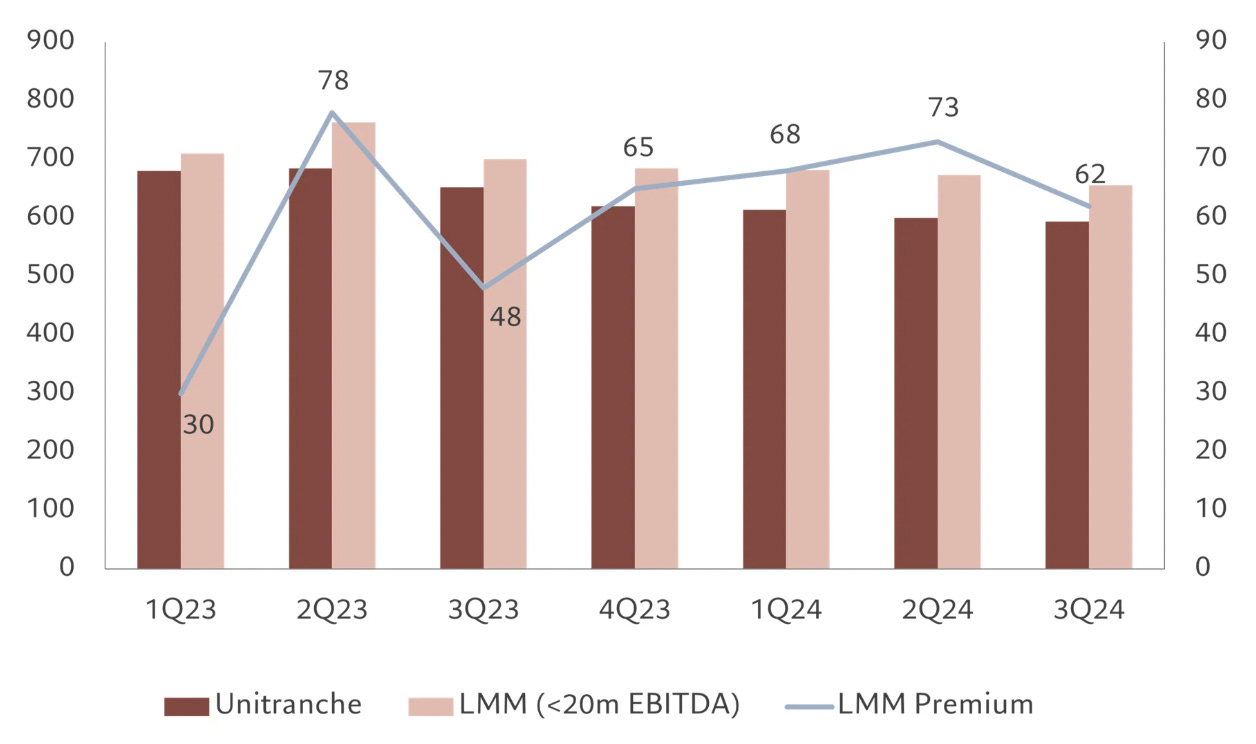

European Private Credit AUM has Grown at a Faster Rate than the US

Spreads on European direct lending deals have tightened over the last year. Core and upper mid-market segments have seen margins come in by close to 100 basis points since early 2023, dipping below the 600 basis point mark for the first time.

Pictet has even seen some Upper mid-market deals close in the 450-500 basis points over base range, often without the benefit of covenants.

Yet in the lower mid-market – EBITDA of up to €15 million – the margin compression has been slightly more modest, at around 20 basis points.

Lower Mid-Market Margin Compression has been Modest

While spreads remain more stable, risk parameters continue to moderate. Leverage, for example, is declining, with more and more deals being closed below four times debt-to-EBITDA and the prevalence of covenants is high.

Pictet expects these contrasting dynamics to continue in 2025, with the lower mid-market remaining a superior and more stable source of income and capital preservation.

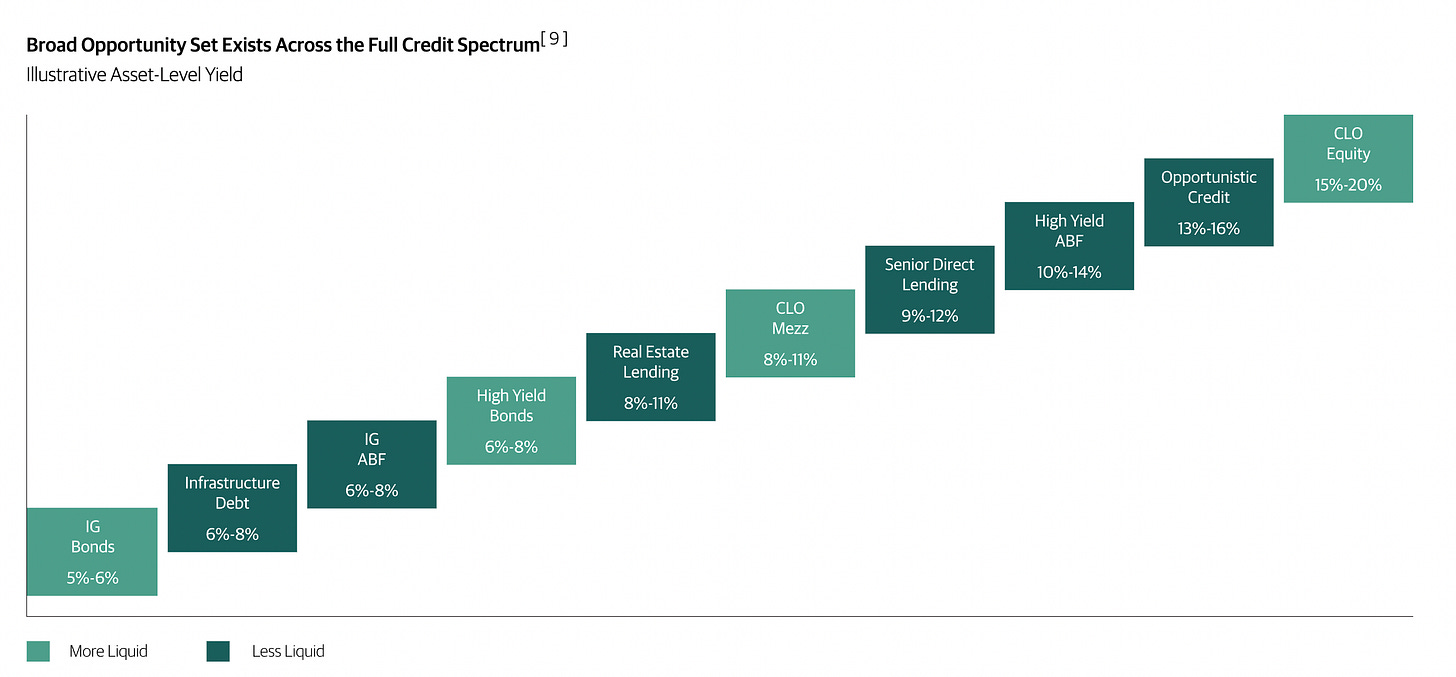

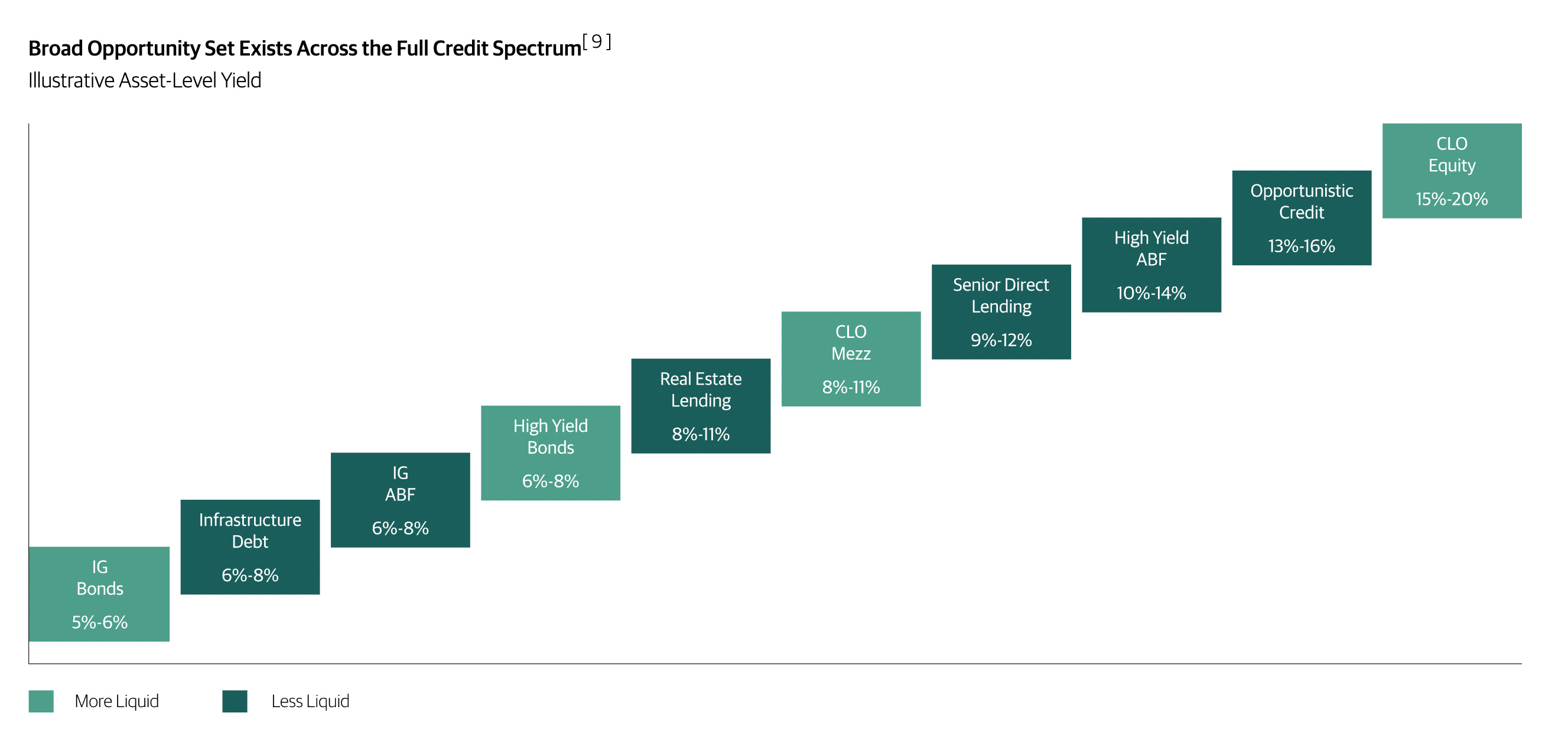

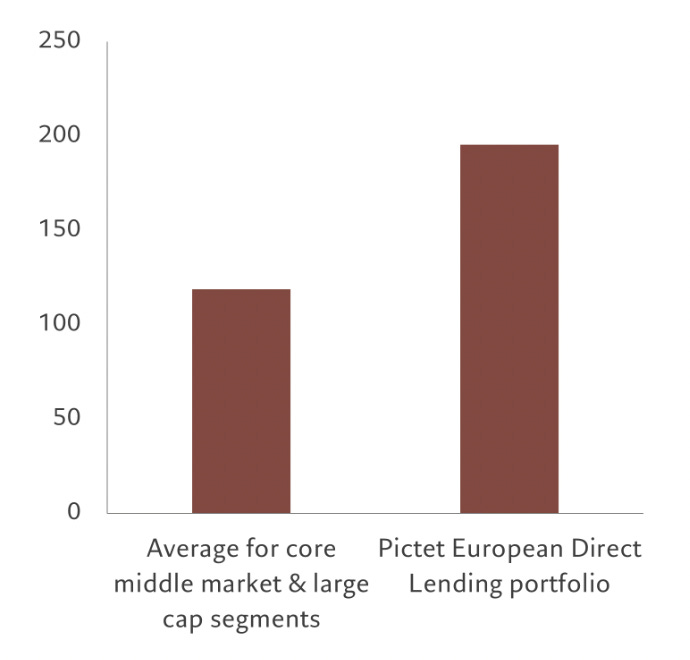

Lower Mid-Market Offers Greater Spread per Turn of Leverage, Bps

💰Fundraising News

Oaktree closed its $16 billion Opportunities Fund XII. The fund invests across both public and private credit and targets a net IRR of 16% to 22%, on an unlevered basis. It has invested or committed more than $7 billion to date. More here and here

Morgan Stanley IM held the fourth close of its $3.2 billion North Haven Private Income Fund. The BDC was launched in February 2022 and lends senior secured loans to sponsored mid-market companies. The fund has invested $7.3 billion in 304 portfolio companies. More here

Goldman Sachs Asset Management is raising up to $3 billion for its West Street Climate Credit Fund. The strategy will target businesses in sectors such as clean energy and sustainable transportation, with an emphasis on North America and Europe. GSAM has committed $150 million to the fund, which will primarily target senior lending opportunities but retain the flexibility to provide junior debt when needed. The fund aims to generate net returns of 8% to 10% on an unlevered basis, with levered investments expected to deliver around 13%. More here

Antares Capital, a Chicago-based alternative credit manager, launched its $1.4 billion Antares Private Credit Fund. The public, non-traded BDC invests primarily in senior secured floating rate loans to sponsored U.S. middle-market companies. Founded in 1996, Antares manages $80 billion of capital under management. More here

Learn more about BDCs here

Invesco Private Credit, an Atlanta-based credit platform, closed its $1.4 billion Lending Fund II. The fund originates senior secured loans of sponsored, core middle market companies primarily in North America (EBITDA of $20-75 million). More here

Bain Capital, closed its $1 billion Middle Market Credit 2022 Fund. The fund finances businesses with EBITDA between $10 million and $150 million located in North America, Europe, and Asia Pacific. It invests across the capital structure. Bain Capital manages~ $11 billion of capital. More here

This newsletter is for education or entertainment purposes only. It should not be taken as investment advice.