OPERS on Private Credit: Three core themes investors should focus on

Fundraising from PGIM, Eiffel Investment, GCM Grosvenor and Equita Capital

👋 Hey, Nick here. A special welcome to the new subscribers at HPS Investment Partners. As a reminder, Golub is the leading subscriber of The Credit Crunch 🥳 Share this with your colleagues to knock Golub off the top spot.

If you’re new, this is the 70th edition of my weekly newsletter. Each week I write about private credit insights and fundraising announcements. You can read my previous articles here and subscribe here. Scroll to the bottom, if you’re here for the fundraising news.

📕Reads of the week

KKR: Why ABF is gaining more attention Link

US Pension Funds are concerned about Private Credit Link

Top Takeaways from Oaktree’s 2024 Link

I hear people say early innings... I think we're still in batting practice. Blackstone thinks Private Credit will grow to $25 trillion. Link

Golub Capital Middle Market Report Link

AXA IM raises $2.5 billion to invest in bank risk transfers Link

Podcast🎧 Howard Marks: Oaktree Capital, Investment philosophy, risk and randomness: Link

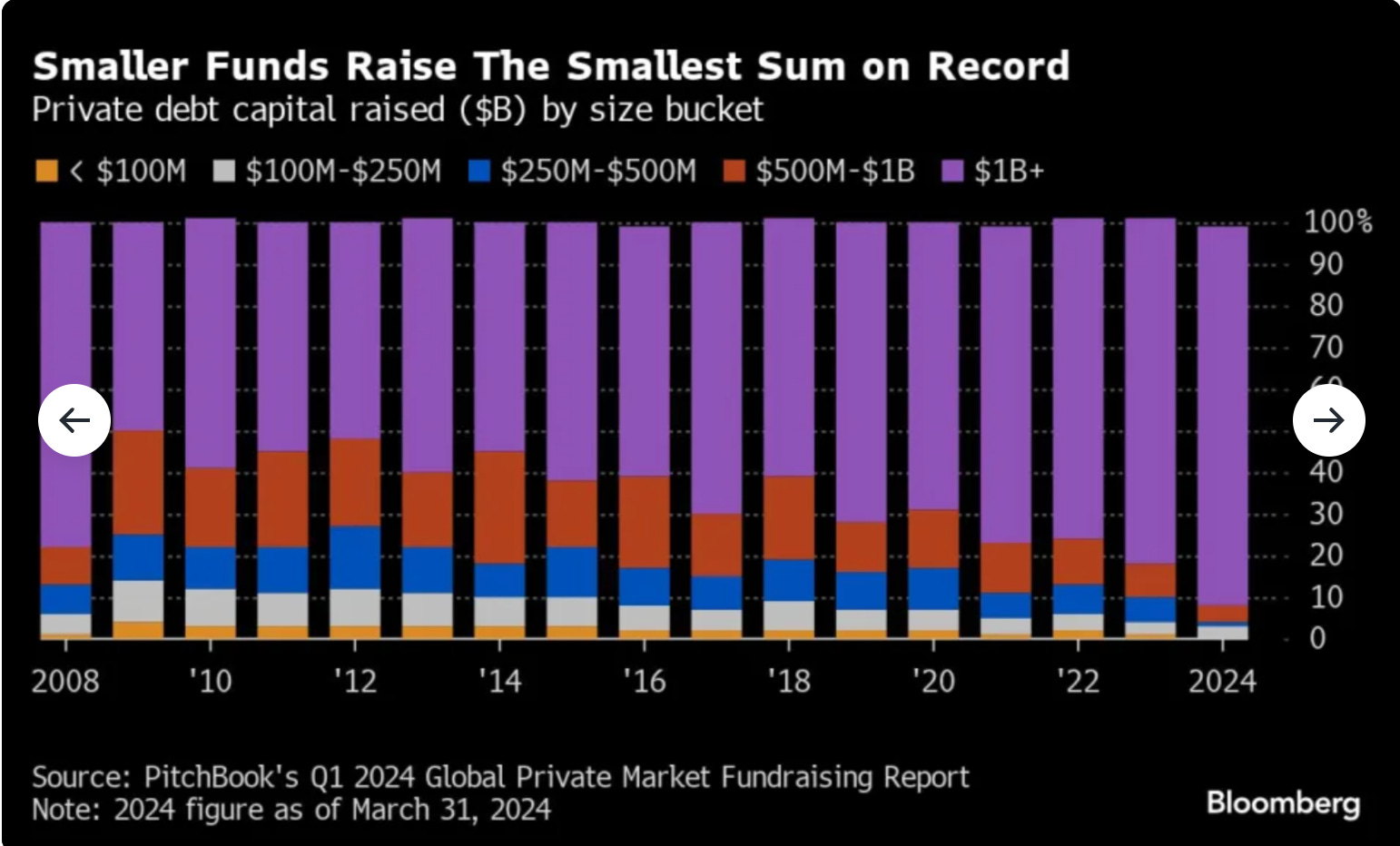

📊Chart of the Week: Private Credit is becoming more concentrated.

Funds with less than $1 billion of assets received the least amount of cash on record last year. Link

OPERS on Private Credit: Three core themes investors should focus on

Ohio Public Employees Retirement System (OPERS) manages $101.8 billion, making it the 12th largest public retirement system in the country. OPERS approved a 1% allocation to Private Credit in January 2023. Despite this target, it expects to take many years to reach its full allocation and is targeting a 0.3% allocation by December 2024.

I recently discovered the OPERS Chief Investment Officer’s, Paul Greff, 2024 investment plan. I’d highly recommend reading below to learn how OPERS is thinking about private credit (Link to the full report here):

Market disruptions created a new area of activity in 2023.

Subordinated debt and preferred equity investments picked up as some senior lenders and common equity holders were reluctant to provide further financing or capital due to market uncertainty.

Senior lenders pulled back on how deep they would lend in a capital structure (approx. 6.5x to 5.0x) and sponsors or common equity holders were either fatigued, capped by concentration limits or reluctant to provide further equity support.

This is an area that NEPC has identified as being particularly attractive and a timely opportunity. Another pocket of activity is the increase in structured with payment-in-kind (“PIK”) features as companies/sponsors sought to conserve cash and preserve liquidity.

We are focused on three general themes in the private debt market.

Theme 1: There is potential for better risk-adjusted returns for floating rate strategies due to higher spreads, borrowers having lower leverage levels and deals having tighter documentation. However, we encourage investors to look at managers with smaller, cleaner existing portfolios and historical workout capabilities. Strategies that diversify away from directly originated corporate debt including asset-based lending have demonstrated some attractive dynamics.

Theme 2: Widespread defaults have not yet occurred; however, indications point towards trouble ahead. Increased interest expenses, coupled with potentially depressed corporate profit margins, is expected to put pressure on liquidity and coverage ratios. Opportunistic, distressed and structured capital strategies could become more attractive. Opportunities specifically in areas such as structured capital and regulatory capital relief have emerged as compelling this year as well.

Theme 3: Continue to commit to private debt managers, even if it means writing smaller checks in this environment. When evaluating new funds, place emphasis on a managers’ sourcing, deal structuring and restructuring/workout capabilities.

💰Fundraising news

PGIM, the asset management arm of Prudential Financial, launched its first ~$500 million Australian real estate debt fund. The fund will provide a mix of senior construction and development loans as well as junior debt and transitional real estate financing. It expects net returns of between 9% and 11% a year. More here

Eiffel Investment Group, a Paris-based asset manager, launched its ~$440 million Impact Direct Lending fund. The fund will finance European SMEs to accelerate their energy transition. It focuses on European SMEs with EBITDA between €5 and €15 million. Facilities are expected to range from €10 to €30 million. The fund will finance ~25 companies. More here

GCM Grosvenor, a Chicago-based asset manager, is set to launch a dedicated private debt secondaries fund. GCM registered the fund with the SEC last month, according to Secondaries Investor. More here

The private debt secondaries market has been targeted by several large asset managers in recent months. JP Morgan said that it expects more than $30bn of private credit to change hands in the secondary market this year, up from just $3bn in 2019. In January, Apollo said that it was looking to raise $2bn for its second credit secondaries fund.

Equita Capital, an Italy-based asset manager, announced a first close of ~$110 million for its Green Impact Fund. The fund invests in renewable infrastructure focusing on solar, wind, and biogas. Equita invests in Italy but can also invest in the rest of Europe - in particular Spain, Greece, and the Nordic countries. More here and here

This newsletter is for education or entertainment purposes only. It should not be taken as investment advice.