Howard Marks revisits the relationship between Debt and Volatility

Fundraising from Avenue Capital, Benefit Street Partners, Quantum Energy Partners, DunPort and Beechbrook

👋 Hey, Nick here. If you’re new, this is the 60th edition of my weekly newsletter. Each week I write about private credit insights and fundraising announcements. You can read my previous articles here and subscribe here. Scroll to the bottom, if you’re here for the fundraising news.

📆 Event of the week - Q124 Middle Market Lending Update

I’ve covered The Configure Partners’ Quarterly several times (Most recently Here).

The team carries out quarterly surveys on private credit lenders as well as tracking data and market insights from debt advisory engagements.

Their latest webinar is next week and I’d highly recommend registering.

In addition to the presentation, this event features a Q&A session. You can submit any questions before the webinar.

Register for the May 22nd webinar here.

📖 Revisiting Volatility and Debt: Howard Marks ft Morgan Housel

This is a summary of Howard Mark’s and Morgan Housel’s articles. You can read the full articles (Here, Here, and Here)

Japan has 140 businesses that are at least 500 years old. A few claim to have been operating continuously for more than 1,000 years.

These ultra-durable businesses are called “shinise,” and studies of them show they tend to share a common characteristic: they hold tons of cash, and no debt.

Does that mean debt is a bad thing and should be avoided? Absolutely not. Rather, it’s a matter of whether the amount of debt is appropriate.

The amount of leverage that it’s prudent to use is purely a function of the riskiness and volatility of the assets it’s used to purchase. The more stable the assets, the more leverage it’s safe to use. Riskier assets, less leverage. It’s that simple.

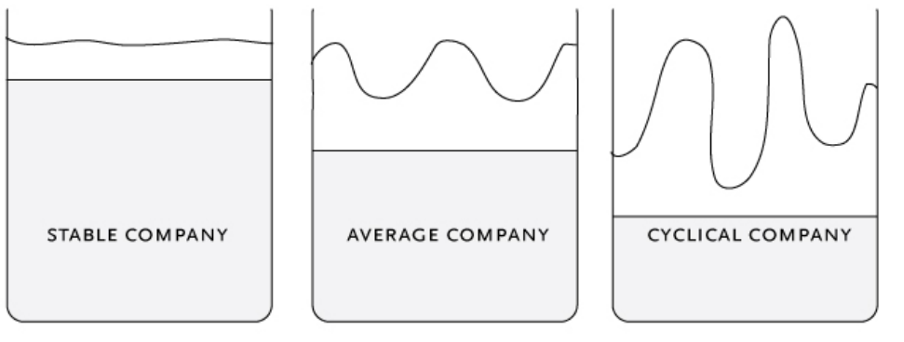

The drawings below show the value of companies of different types. Due to the variability of their earnings, the values fluctuate differently over time

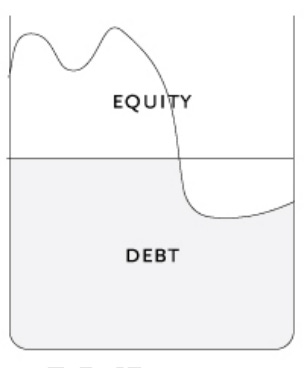

Here’s a financial structure, except with the equity above the debt, not below as it would be on a balance sheet:

Now let’s combine the two concepts. In order for a company to avoid insolvency, its value can’t fall through the equity and into the debt. When the amount of debt exceeds the value of the company, it’s insolvent, as suggested below.

What the following doodles illustrate is that for every level of riskiness and volatility, there’s an appropriate limit on leverage in the capital structure

Extremely leveraged companies have existed for more than a century. They’re called utilities. Because their profits are regulated by public commissions and fixed as a percentage of their stable asset bases, they’ve been extremely dependable. This shows that high leverage isn’t necessarily risky, just the wrong level of leverage given the company’s stability.

The reason for taking on debt is simple: to increase so-called capital efficiency. Debt capital is usually cheap relative to the expected returns that motivate equity investments and thus relative to the imputed cost of equity capital. Thus, it’s efficient to use it in lieu of equity.

The problem is that extreme volatility and loss surface only infrequently. And as time passes without that happening, it appears more and more likely that it’ll never happen – that assumptions regarding risk were too conservative. Thus, it becomes tempting to relax rules and increase leverage. And often this is done just before the risk finally rears its head. As Nassim Nicholas Taleb wrote in Fooled by Randomness:

Reality is far more vicious than Russian roulette. First, it delivers the fatal bullet rather infrequently, like a revolver that would have hundreds, even thousands of chambers instead of six. After a few dozen tries, one forgets about the existence of a bullet, under a numbing false sense of security . . . Second, unlike a well-defined precise game like Russian roulette, where the risks are visible to anyone capable of multiplying and dividing by six, one does not observe the barrel of reality. . . . One is thus capable of unwittingly playing Russian roulette – and calling it by some alternative “low risk” name.

The most important adage regarding leverage reminds us to “never forget the six-foot-tall person who drowned crossing the stream that was five feet deep on average.”

As with so many aspects of investing, determining the proper amount of leverage has to be a function of optimizing, not maximizing. Given that leverage magnifies gains when there are gains and that investors only invest when they expect there to be gains, it can be tempting to think the right amount of leverage is “all you can get.” But if you bear in mind (a) leverage’s potential to magnify losses when there are losses and (b) the risk of ruin under extreme negative circumstances, investors should usually use less than the maximum available. Successful investments, perhaps enhanced by the moderate use of leverage, should usually provide a good-enough return – something few people think about in good times.

Clearly, it’s difficult to always use the right amount of leverage, because it’s difficult to be sure you’re allowing sufficiently for risk. Leverage should only be used on the basis of demonstrably cautious assumptions. And it should be noted that if you’re doing something novel, unproven, risky, volatile, or potentially life-threatening, you shouldn’t seek to maximize returns. Instead, err on the side of caution. The key to survival lies in what Warren Buffett constantly harps on: margin of safety.

The right way to think about debt may be best captured by one of the oldest maxims:

“There are old investors, and there are bold investors, but there aren’t many old bold investors.”

Using a moderate amount of borrowed capital balances the desire for enhanced gains against the awareness of the potential negative consequences. It’s only in this way that one can hope to attain the longevity of Morgan Housel’s 500-year-old success stories.

💰Fundraising news

Avenue Capital, a New York-based investment manager, closed its $1 billion Europe Special Situations Fund V. The fund lends senior secured, asset-backed loans to companies in Northern Europe. It focuses on small and middle-market loans to both sponsored and non-sponsor-backed borrowers. Avenue has invested more than $26bn in European credit and special situations. More here

Benefit Street Partners, a New York-based alternative asset manager, closed its $850 million Special Situations Fund II. The Fund invests in stressed and distressed investments in four categories: non-market correlated opportunities, low loan-to-value credit, high yield debt and restructuring opportunities. The fund will focus on North American companies with sub $1.5 billion debt capital structures. It targets net returns of 15–20%+IRR and a 2.0x – 2.5x MOIC. More here and here

Quantum Energy Partners, a Texas-based private equity firm, is raising a $2.25 billion Energy Credit fund. It will have two sleeves: a $1.5 billion tranche for lending to oil and gas producers and a further $750 million for companies supporting the transition away from fossil fuels. More here

DunPort Capital Management, an Ireland-based asset manager, announced a ~$63 million co-investment vehicle with the British Business Investments. The fund will lend to UK-based businesses with a revenue of less than £100m. It will co-invest alongside Dunport's main fund, Oak Corporate Credit DAC. More here

Beechbrook Capital, a London-based credit manager, announced a $25 million co-investment vehicle with the British Business Investments. The fund invests in SMEs with revenue between £10m and £100m, and an EBITDA of £1m and above. It lends senior secured loans to private, non-sponsored companies. Since 2008, Beechbrook has invested more than £0.5bn in 70 companies across the UK. More here