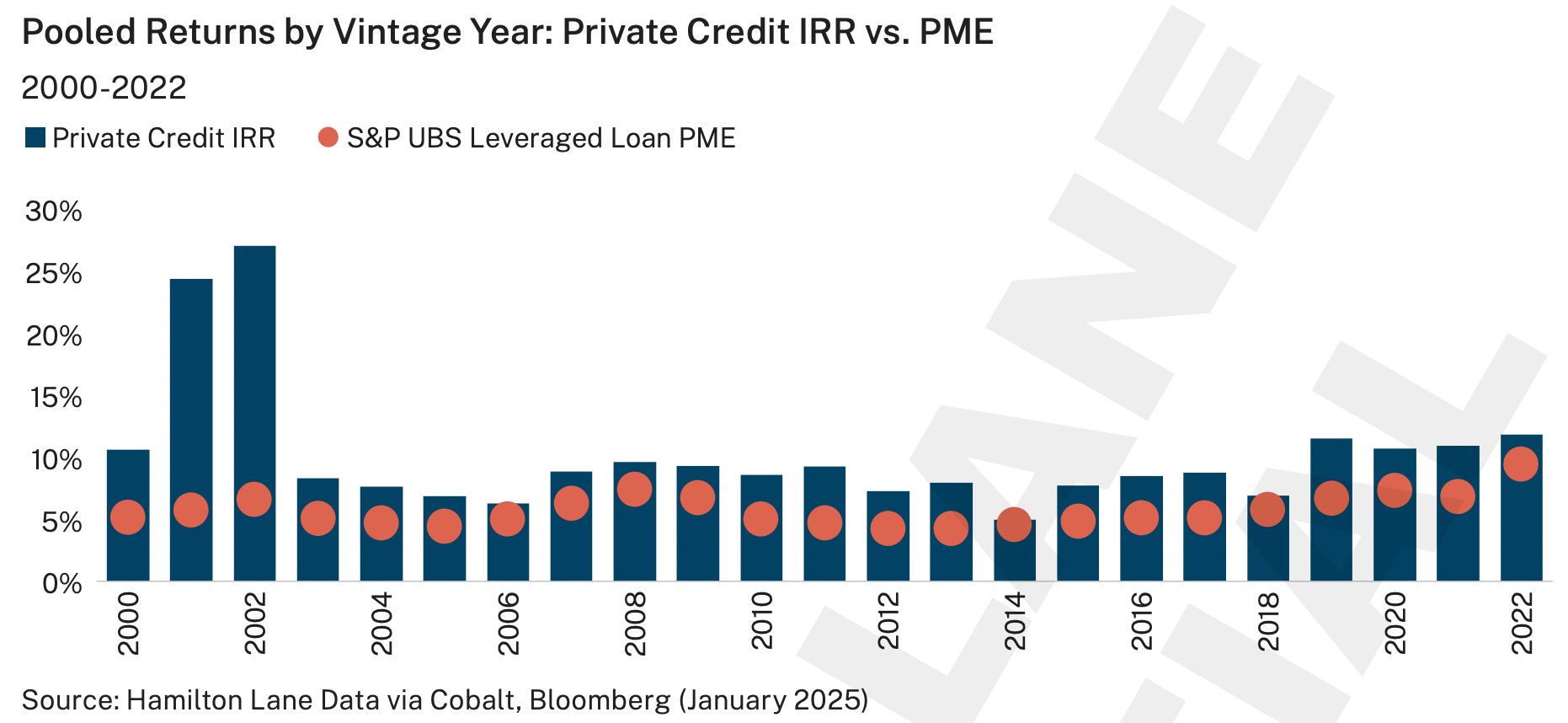

Hamilton Lane: Private credit has outperformed public credit for 23 years running

Fundraisings from Marathon Asset Management, ICG, Goldman Sachs Alternatives, Arcmont and Liquidity.

👋 Hey, Nick here. A special welcome to the new subscribers from Alternative Fund Advisors, FM Global and Upper90

It’s great to have you. Reach out and say hi. This is the 106th edition of my weekly newsletter. Each week, I write about private credit insights and fundraising announcements. You can read my previous articles here and subscribe here

📕 Reads of the Week

Pitchbook: The broadly syndicated market is gunning for the biggest chunks of private credit loan books. Lenders are proactively cutting spreads in a bid to prevent their companies from refinancing in the broadly syndicated market Link

BlackRock outspends its rivals in the race to build private market arms. Link

CVC Eyes US Private Credit in Expansion Drive. Link

Private Credit Firms Are Pushing Boundaries to Win Large Deals: Leverage can stretch to eight times debt-to-earnings, and for some deals, above 10. Terms have loosened, too, with more lenders accepting a lack of maintenance covenants and generous EBITDA definitions. Link

Blue Owl's direct lending strategy accounts for over half of $1 billion Asia fundraise. Link

Castlelake closes its fifth aviation-focused credit fund with more than $2 billion in committed capital. Link

FT Alphaville: Is credit cruising for a bruising? Between 2014 - 2024 The share of BBs, the highest-rated portion of the index, has climbed from 41% to 51% of the high-yield index. The high-yield market has gotten safer as private markets have removed risky borrowers from high yield and expanded the pool of risky borrowers in the private credit market. Link

Nomura: Covenant protection is being gradually diluted to the point of almost being meaningless… I also think it’s unavoidable given the weight of capital that’s sitting on the sidelines and needs to earn fees by being deployed. Link

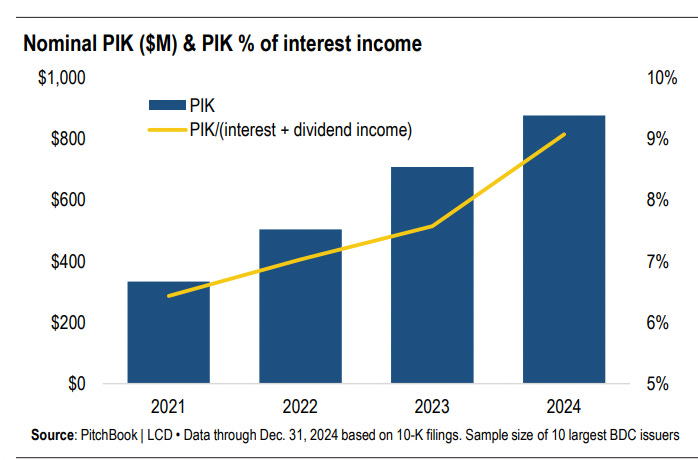

BDCs utilization of PIK continues to climb Link

🏦 Partnerships of the Week

Silicon Valley Bank and Pinegrove Venture Partners Announced its Lending Partnership. SVB and Pinegrove expect to deploy $2.5 billion in venture debt loans to technology and life science companies over the coming years. More here

Lincoln Financial, a US annuity provider, partnered with Bain Capital and Partners Group. Bain Capital will provide access to a varied portfolio of private credit investments, including direct lending, asset-based finance, and structured credit. Partners Group will launch an evergreen fund focusing on a cross-sector private markets royalty portfolio. It will invest across well-established royalty sectors, such as intellectual property assets in the pharmaceutical and entertainment industries, and emerging high-growth sectors like energy transition, sports, and brands. More here

DWS and Deutsche Bank announced its private credit partnership. DWS will have preferred access to certain asset-based finance, direct lending, and other private credit asset opportunities originated by Deutsche Bank. More here

📊Hamilton Lane 2025 Market Overview

Hamilton Lane published its 2025 Market Overview. Its clarity of thought and sharp editorial tone make it a compelling read. While the report focuses primarily on private equity, it offers several valuable insights relevant to private credit.

If you're short on time, here are the key highlights—but the full report is well worth a read. Link

Private credit has outperformed public credit for 23 straight years

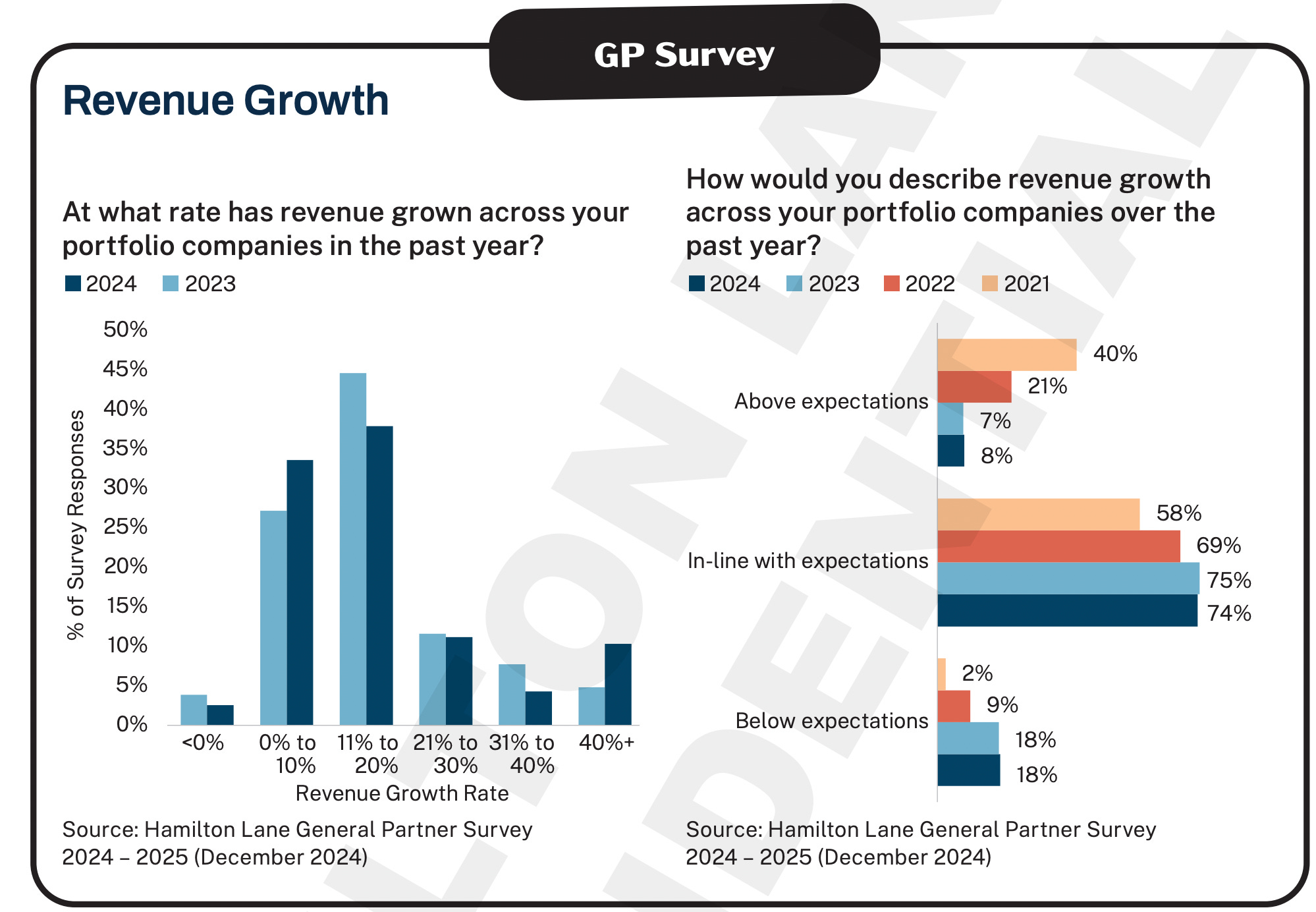

GPs Expect Modest Revenue Growth

This is in line their portfolio performance over the last two years

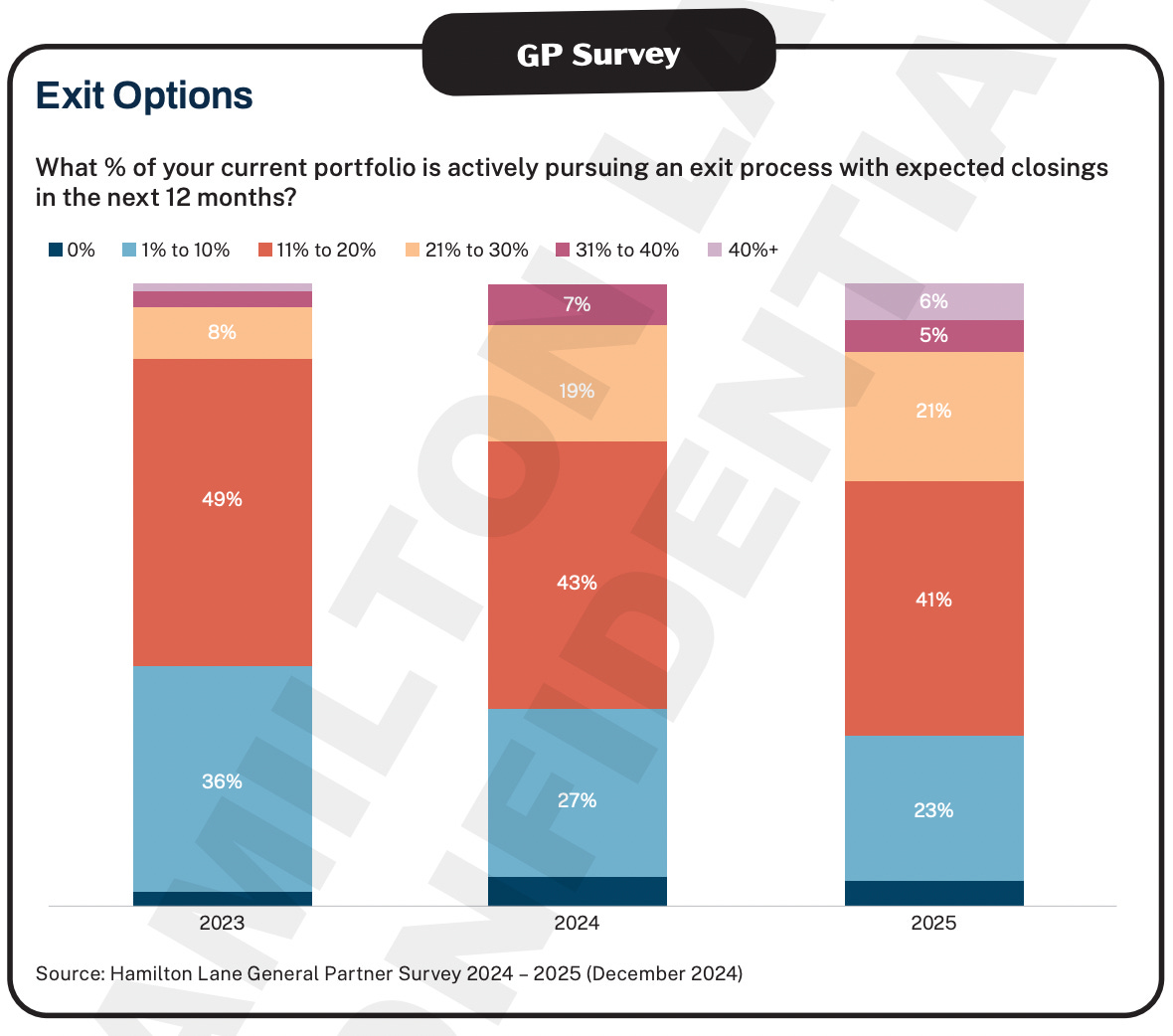

We’re seeing a significant rise in the number of companies preparing for exit.

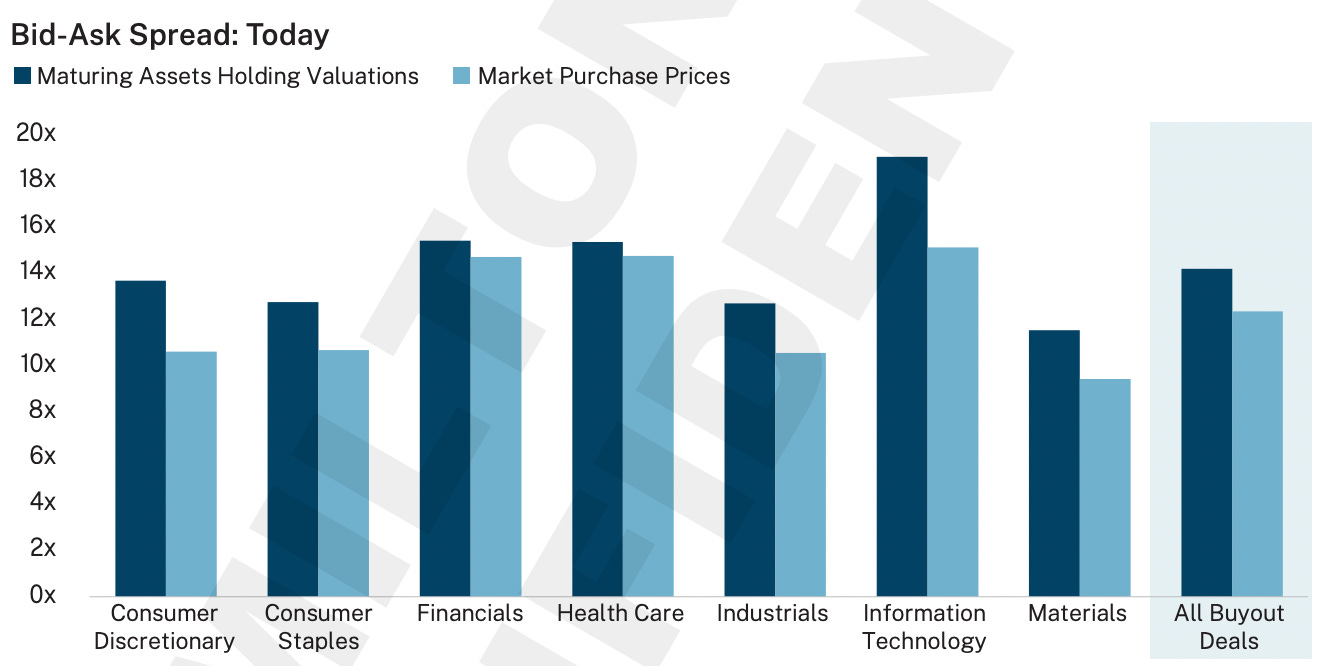

Portfolio companies acquired in 2019/20 are still marked at higher valuations than more recent deals from 2022/23

In every category.

Deal activity is low for one fundamental reason.

Buyers and sellers cannot agree on a clearing price for their companies.

If you’re a seller, revenue and earnings are good, the markets and comparable assets are strong and there’s no reason you want to accept any discount to what you believe the asset is worth.

If you’re a buyer, you don’t want to pay that value because you aren’t sure what the future holds, and you don’t want to pay a full price for what could end up being peak earnings for that asset you are buying.

Read the full report here

💰Fundraising News

Marathon Asset Management closed its $2.7 billion global opportunistic credit strategy. The fund focuses on direct origination of private capital opportunities, both as growth capital and in more complex situations across the credit landscape. MDCF I closed in 2020 and so far has achieved a DPI of 65%. More here

ICG, a London-based manager, closed its $3.3 billion European Mid-Market Fund II, a 300% increase compared to the prior fund. The fund has already made seven investments and is 35% deployed. MMF I closed in late 2018 and so far has achieved a DPI of 71%.

Goldman Sachs Alternatives launched its Climate Credit strategy. The strategy has already raised $1 billion. The strategy will provide tailored solutions to climate and environment-related businesses. It is senior-focused but can invest across the capital structure. More here

Arcmont, a London-based credit manager, has secured ~$520 million for its new Impact Lending strategy. The strategy finances companies that address critical environmental and social challenges. It focuses on four key themes: climate, health, education, and sustainable economic growth. The firm has partnered with Bridgespan Social Impact to develop its approach. More here

Liquidity, a London-based growth lender, raised $450 million. The funds will support the expansion of Liquidity’s lending capabilities in the US market. Liquidity originates, underwrites, and monitors investments using an in-house AI. It typically lends $10 million to $150 million to growth-stage tech companies. More here

This newsletter is for education or entertainment purposes only. It should not be taken as investment advice.