Ares Alternative Credit on Data Centers

"We don’t think that generating excess returns in this sector will be especially easy".

👋 Hey, Nick here. Last week, I rewatched, The Pursuit of Happyness, one of my all-time favorites. A scene that really stuck with me was when Chris Gardner’s son shared The Parable of the Drowning Man. (Watch the scene here).

After reading two memos this week, In the Gaps and Howard Marks, I can’t help but feel that this parable is playing out in private credit markets.

The pressure to deploy can blind us from the risks we should be pricing in. But if the ‘credit gods’ are sending warnings, do we listen—or do we convince ourselves that another boat will come?

A special welcome to the new subscribers from OPERS, Prosek Partners, Nomura, and Pitchbook. It’s great to have you. Reach out and say hi. This is the 104th edition of my weekly newsletter. Each week, I write about private credit insights and fundraising announcements. You can read my previous articles here and subscribe here

📕 Reads of the Week

Howard Marks Memo: Are today’s spreads sufficient to offset the future credit losses? Link

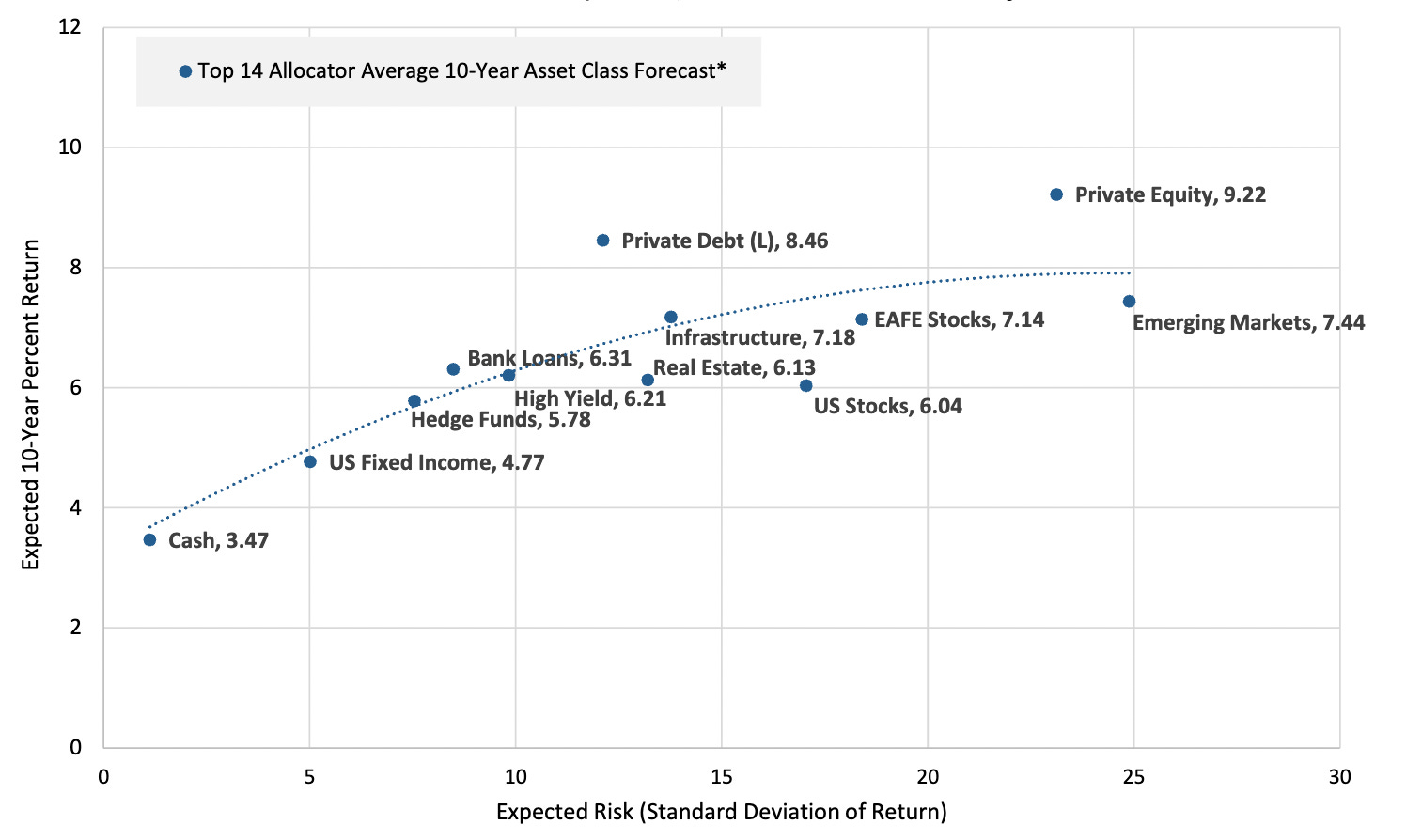

Cliffwater: Private credit and private equity should expect continued inflows at the expense of public equity and private real estate. This report is based on a survey of 14 of the largest allocators/advisors. Link

Blue Owl Cuts Fees for Early European Private Credit Investors. Link

Mckinsey Global Markets Report: Buyout leverage of 4.1 times remains below the ten-year average of 4.2 times and well below the 4.7 times high in 2021. Link

🎧 Deal Catalyst: The Credit Clubhouse Podcast. Link

🎧 AllianceBernstein: Private Debt Will Keep Its Edge. Link

“Most of US private credit managers are challenged in their struggle to differentiate.”

Pitchbook’s Q1 Global Private Credit Survey: Link

📈Charts of the Week

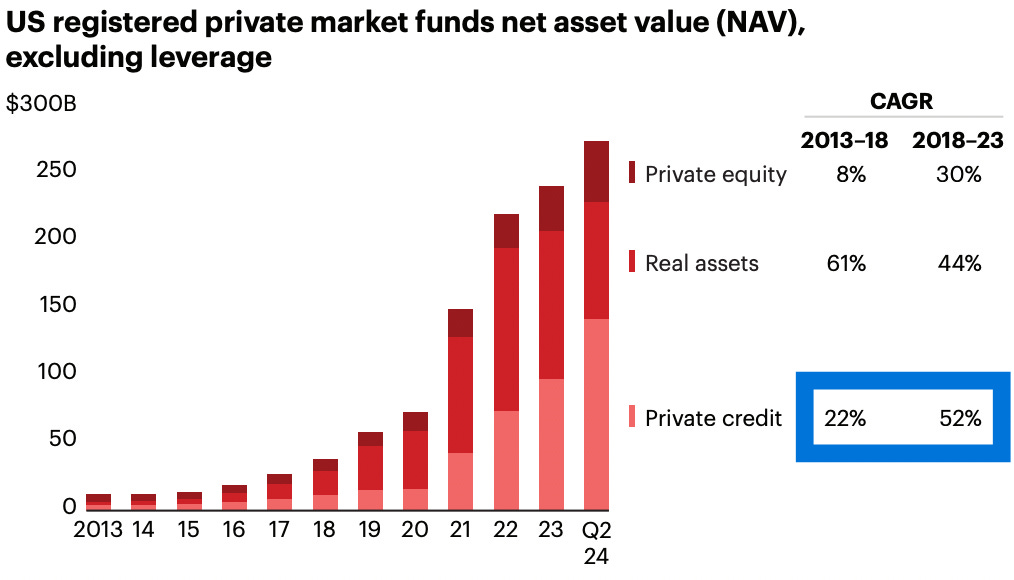

US Private Credit Retail Funds Have Shown Strong Growth over the Past Decade

Cliffwater’s Consensus 10-Year Expected Return and Risk

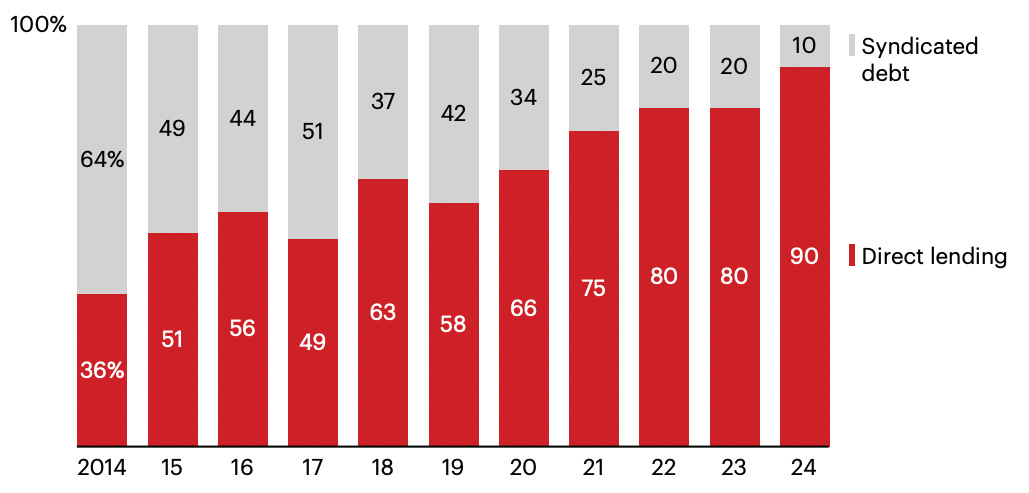

Direct Lending Accounts for 90% of US Buyout Loans

🏦 Partnerships of the Week

Blackstone Credit & Insurance made a minority investment into ITE Management, an alternative manager focused on transportation infrastructure. The partnership also includes a forward flow partnership, with Blackstone aiming to invest up to $2 billion. More here

PIF agreed to anchor Goldman Sachs Asset Management’s Saudi Arabia funds. The private credit strategy will lend to companies in the GCC region or do most of their business with the region. More here

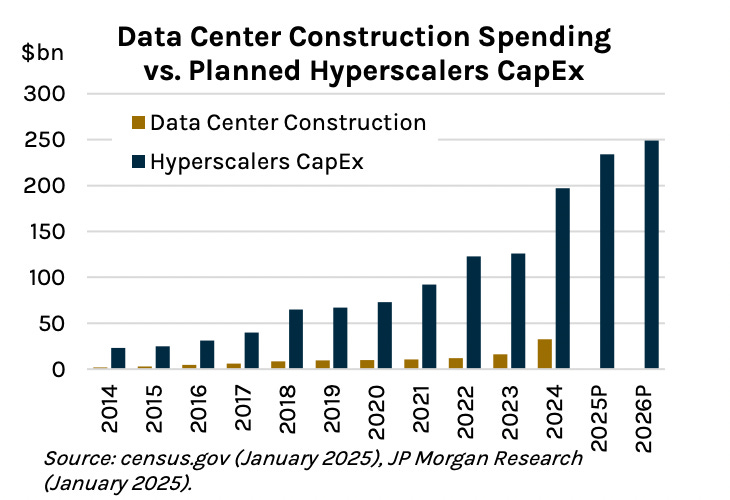

💻 Ares Alternative Credit: In the Gaps Winter 2025

A few months ago, I wrote a piece about In the Gaps, a newsletter by the Ares Alternative Credit team. The team recently published its latest edition, and it didn’t disappoint. Below is a condensed version of their insights on financing data centers. If you're interested in how leading credit investors are thinking about data center financing, it's worth reading the full newsletter here.

In the U.S., where around half of all data centers are located, data center power usage is expected to double by 2027.

Just to power U.S. data centers, the equivalent of New York City’s worth of energy capacity needs to be added every year.

Wait times for newly built data centers to be connected to power over four years (compared to 18 months historically).

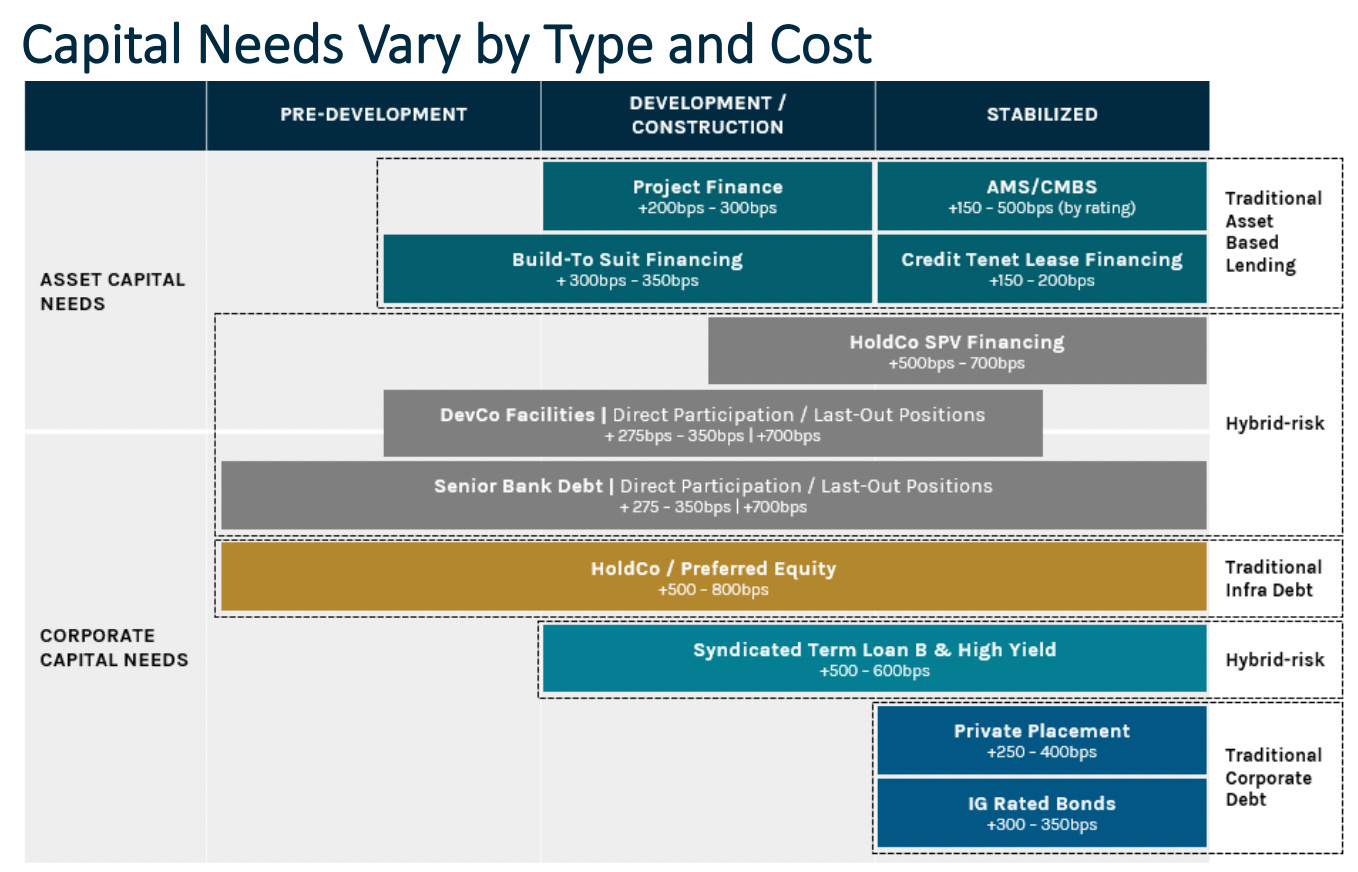

The capital needs for all of this are, to say the least, equally daunting. There is not nearly enough capital

A wide variety of different types of capital and strategies, in scale, will be required.

Some of the capital needs involve hybrid risks: some combination of two or more traditional financing solutions (e.g., assets, infrastructure, real estate and corporate).

Traditional pools of capital are likely to struggle to provide these hybrid-risk capital solutions due to either mandate restrictions or platform limitations.

The overall infrastructure investment gap is estimated to be $1.6 trillion through 2030.

Despite the construction growth of the last few years, demand for data centers is multiples greater

Generating excess returns in this sector won’t be especially easy

The spectrum of risks will vary in the extremes from VC-like risk in the earliest stages to re-leasing and technology obsolescence risk in the later stages of these assets. Therein lies the reason to proceed with caution.

Ares believes that some of the greatest mistakes that will be made in this sector will be associated with hybrid-risk transactions.

Traditional, “pure-play” investors may find themselves ill-equipped to underwrite all facets of a hybrid-risk transaction.

Asset-based credit investors are likely to play their most significant role downstream from where development and construction risks are more pronounced.

By focusing on assets already built and generating stable, contractual cash flows, one can reduce (but certainly cannot eliminate) some of the most challenging risks to evaluate.

Success in these transactions will require deep platform integration and collaboration, something that many firms struggle to achieve.

This is a great reminder of one of my favourite In the Gaps lessons.

Lesson 2 - Buy assets and cash flow, the rest is noise: FOMO on the “next big thing” is often the pathway to the next big bubble. In credit, we are measured not by our wins but by avoiding losses. We believe sticking to fundamentals and ignoring the noise is the only path to long-term returns. While compounding has been called the eighth wonder of the world, it can’t overcome high severity losses (which often begin by ignoring rule 2).

Once again, read the full newsletter here. Thanks again to Joel Holsinger and the rest of the Ares Alternative Credit team for publishing this.

💰Fundraising News

Blackstone announced a final close of $ 8 billion for its Real Estate Debt Strategies V.

The fund invests globally, deploying capital across several strategies, including global scale lending, liquid securities, structured solutions to financial institutions, and corporate credit. Blackstone Real Estate Debt Strategies has $77 billion of assets under management and over 170 professionals globally. More here

Brookfield Asset Management plans to raise at least $7 billion for its fourth infrastructure debt fund. Its predecessor, which closed in November 2023 with over $6 billion, is now largely deployed. During its recent earnings call, Brookfield emphasized that its infrastructure debt platform is already the largest strategy of its kind, and the upcoming fund is expected to be substantially larger than the previous one. More here

400 Capital Management, a New York-based alternative credit manager, closed its $1.4 billion Asset Based Term Fund IV. The fund invests in public and private credit markets in the U.S. and Europe. They invest primarily in residential real estate, commercial real estate, consumer finance, and specialty finance markets. More here

Northleaf Capital Partners, a Canada-based alternative manager, closed its $1 billion Northleaf Private Credit III fund. The fund will lend globally to sponsored mid-market companies as well as invest in asset-based specialty finance portfolios. It has the flexibility to invest in senior and junior loans. More here

Lane42, a Los Angeles-based alternative manager, launched its $2 billion investment platform. The manager is founded by Former Ares partner, Scott L. Graves, and will invest in both public and private markets. More here

Octopus Investments, a UK-based investment manager, launched its ~$1 billion Real Estate Debt Fund IV. The fund will lend senior-secured acquisition, development, and stabilisation loans across the UK. It will focus on living sectors but will have an allocation to offices, industrial, and retail. More here

Legacy Corporate Lending, a Dallas-Fort Worth-based manager, announced its launch as an independent lender. The launch is backed by a significant equity investment from Bain Capital. Legacy provides asset-backed loans to North American mid-market companies. Loans will range from $10 to $40 million and are secured by assets, including accounts receivable, inventory, machinery and equipment, real estate, and intellectual property. More here

Morgan Stanley IM launched a European direct lending fund. The fund will lend senior secured loans to European middle-market companies. Investors can invest via monthly subscriptions and earn monthly income distributions. The fund will also allow quarterly liquidity after a one-year lock-up period. More here

This newsletter is for education or entertainment purposes only. It should not be taken as investment advice.